How Much Money Does It Take To Earn 100000 Per Year In Interest

In the world of early retirees, we take a concept that goes by names like "The 4% rule", or "The iv% Safe Withdrawal Rate", or just "The SWR."

As with all things financial, information technology's the subject of plenty of controversy, and nosotros'll get to that (and and then dial information technology flat) later. But for now, for those new to the concept, allow's define the Safe Withdrawal Rate:

That sounds overnice and simple, merely many people consider it an unpredictable thing to nail down.

After all, yous don't know what sort of rollercoaster rides the economy will accept your retirement savings on, and you too don't know what rate of inflation will persist through your lifetime. Volition a box of eggs cost $6.00 a dozen when y'all're 65, or will it be closer to $lx? So how can nosotros possibly know how much money nosotros volition need to alive on in retirement?

The answers you lot get to this question vary widely.

Financial beginners (well-nigh 95% of the population) tend to randomly simply throw out a number between v-100 million dollars.

Financial advisers who aren't Mustachians volition tell you that it depends on your pre-retirement income, (with the implicit supposition that you are spending about of what you earn) and the end answer will be somewhere betwixt ii and 10 million.

Financial Independence enthusiasts will take the closest-to-right answer: Have your almanac spending , and multiply it past somewhere betwixt 20 and 30. That's your retirement number.

If you employ the number 25, you're implicitly using a 4% Safe Withdrawal Rate, which is my ain personal favorite number.

So where does this magic number come up from?

At the most basic level, you can think of it like this: imagine you accept your 'stash of retirement savings invested in stocks or other assets. They pay dividends and appreciate in price at a total charge per unit of 7% per year, before inflation. Inflation eats 3% on average, leaving you with 4% to spend reliably, forever.

I tin can already hear a chorus of whines and rattling keyboards starting up, then let's authorize that argument. I acknowledge information technology: that is the idealized and simplified version.

In reality, stocks go upwardly and downwardly every yr, and so does inflation. Over a long multi-decade menstruation like the gigantic retirement you and I will be enjoying, enormous things have happened in the past. The Great Low. The Earth Wars, Vietnam, and the Common cold War. The abandonment of the gold standard for US currency and years of x%+ inflation and 20%+ interest rates. More recently, the groovy financial crash and a slicing in half of of existent estate and stock values.

If you lot happened to retire in 1921 on a mostly-stock nest egg, you would take experienced an enormous stock run-up for the first eight years of your retirement. You'd be then rich by the time the 1929 crash and the Great Depression striking, that you'd barely observe the trouble in the streets from your rosewood-paneled tea room.

On the other mitt, if you retired in early 2000 while holding stocks, y'all saw an immediate and huge drop in your savings along with low dividend yields – and your 'stash may be have had some scary times in the early days, and over again effectually 2009. Would you still have any money left today?

In other words – the sequencing of booms and crashes matters. Ideally, you lot want to reach your magic retirement number in a time of dainty, reasonable stock prices, simply before the starting time of another long boom and so that your retirement starts off on a good human foot. But you can't predict these things in advance. And so over again, how practise nosotros observe the correct answer?

Luckily, diverse Early on Retirement Ninjas have washed the piece of work for us. They analyzed what would have happened for a hypothetical person who spent 30 years in retirement betwixt the years 1925-1955. then 1926-1956, 1927-1957, and so on.

They gave this imaginary retiree a mixture of 50% stocks and 50% v-year US government bonds, a fairly sensible asset allocation. Then they forced the retiree to spend an ever-increasing amount of his portfolio each yr, starting with an initial percentage, and then indexed automatically to inflation as defined by the Consumer Cost Index (CPI).

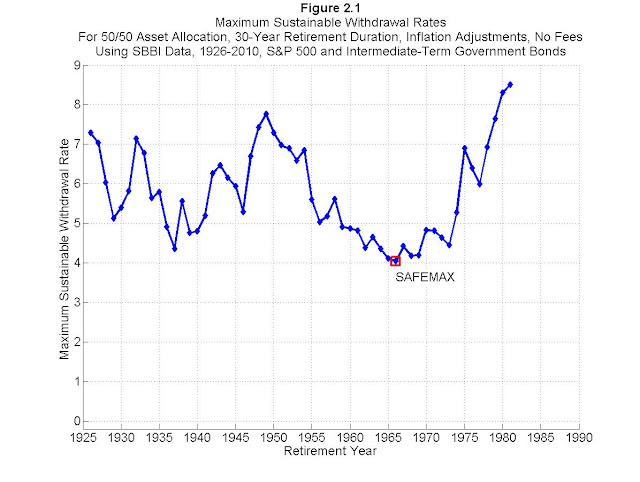

This simple but important series of calculations was chosen the Trinity Study, and since then information technology has been updated, tweaked, and reported on, and it's still the subject of lots of contend today. Wade Pfau is ane reasonable vox in the manufacture, and he created the following useful chart showing what the maximum safe withdrawal rate would have been for diverse retirement years:

Every bit you can see, the 4% value is really somewhat of a worst-example scenario in the 65 year period covered in the study. In many years, retirees could have spent 5% or more than of their savings each year, and still ended up with a growing surplus.

This brings me to a critical point: this report defines "success" as not going broke during a 30-twelvemonth test period. To people similar you and me who volition enjoy lx-year retirements, that would not be successful – we desire our money to concluding much longer than 30 years.

Luckily, the math in this example is pretty interesting: there is very trivial difference betwixt a 30-year period, and an infinite year period, when determining how long your money will last. Information technology's much like a xxx-year mortgage, where almost all of your payment is interest. Driblet your payment by just $199 per month, and suddenly yous've got a thou-year mortgage that volition literally accept y'all 1000 years to pay off. Increase the payment past a few hundred, and you have a fifteen twelvemonth payoff!

In other words, above 30 years, the length of your retirement barely affects the rubber withdrawal rate calculations.

So far, we're liking the iv% rule quite a bit, right? But yet whenever I mention it, I get complaints. Permit's review a few of them:

- The trinity study is based on a prosperity anomaly: the United States during its smash years. Yous tin't project skillful times like that into the future, considering nosotros're just about to enter the Doom Years!

- Economical growth and stock appreciation was all based on inexpensive fossil fuels. How will this all wait after Peak Oil hits us!?

- You can't take a one-size-fits-all rule and utilise it to something equally varied equally an economy and an private'due south life! My wellness care costs could go up! Hyperinflation could strike!

- Even at a 4% withdrawal rate, there's still a take chances of portfolio failure. That ways I'll be flat broke and out on the street in my onetime age. I recommend doubling your savings, and going for a two% SWR instead because there'southward never been a failure in that scenario!

- This is all wrong! Waaah, waaah!

That's all well and good. While there are solid economical analyses that I believe can out-argue the points above, I'one thousand not patient or clever plenty to re-create them here. Pessimists are costless to enjoy their pessimism and even write most it on their ain blogs.

Instead of debating unprovable points like those to a higher place, we tin can completely squash them with our ain much more powerful list of points:

The trinity written report assumes a retiree will:

- never earn whatever more than money through part-time piece of work or self-employment projects

- never collect a single dollar from social security or any other alimony plan

- never adjust spending to business relationship for economic reality like a huge recession

- never substitute appurtenances to recoup for inflation or cost fluctuation (vacation in a closer place one year during an oil price spike, or switch to almond milk in the issue of a dairy milk embargo).

- never collect any inheritance from the passing of parents or other family members

- and never do what almost old people tend to do according to studies – spend less as they age

In short, they are assuming a bunch of drooling Consummate Antimustachians. You and I are Mustachians, meaning we have far more than flexibility in our lifestyles. In short, nosotros have designed a Safety Margin into our lives that is wider than the average person's unabridged retirement plan.

So now that nosotros're feeling good about the 4% rule once again, let'south bring the bespeak home:

Far from existence a risky proffer, planning for 4% Safe Withdrawal charge per unit is actually the most conservative method of retirement saving I could perhaps recommend.

To apply information technology in real life, just take your almanac spending level, and multiply it past 25. That'southward how much you need to retire, at the near. A $25,000 spender like me needs $625,000. I've got more than that, plus various safety margins in the lifestyle, and so all is practiced.

Without undue risk, and every bit long every bit yous have skills that can be used to earn money eventually in the future (hint: you do), I can even advocate an SWR of 5%. In other words, get your expenses down to $25k, and you tin quit your job on $500k or less. Then you tin utilise the methods described in First Retire, then Get Rich to gradually increase your safety margin (and effectively decrease your withdrawal rate) as you historic period.

So there'southward no need to debate. four% is a perfectly adept answer, which means 25 times your almanac expenses is a perfectly good goal to save for. Along the way, you lot might notice your annual expenses melting abroad, which makes things always-more-attainable (equally shown in the shockingly uncomplicated math behind early on retirement post). Merely worry, you must not.

And if yous're ready to play with the numbers fifty-fifty further, check out the FIREcalc website. Information technology's basically like owning your ain Trinity Written report machine, except you can tweak variables (await at the tabs at the pinnacle of the page). In the link provided, I used this data:

- 500,000 portfolio

- 25,000 almanac spending (5% withdrawal rate).

All alone, a plan like that over threescore years of retirement but has a 45% success charge per unit, historically speaking.

Just if you brand adjustments which include:

- $8,000 per year of social security starting near 25 years from now

- "Bernicke'south Reality Retirement plan" of dropping spending slightly with age

- Just $three,000 per yr in fooling-effectually income

You're already at an over 90% success rate. Some other hundred or two dollars per calendar month and yous have a 100% chance of success, even without invoking many of my other bullet points above.

So that, at final is the long-awaited Safe Withdrawal Charge per unit article.

In the hands of financial infants, the rule is dangerous and scary. Only in the hands of Mustachians, zero is scary. Planning for a 4% withdrawal rate is a shiny, bulletproof limousine of a retirement plan and you can ride it all the way to the political party at Mr. Money Mustache's firm.

Source: https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/

Posted by: snyderalludeply.blogspot.com

0 Response to "How Much Money Does It Take To Earn 100000 Per Year In Interest"

Post a Comment